The global race in artificial intelligence is rapidly evolving into a two-player contest between the United States and China. While the U.S. continues to dominate in AI model innovation and chip design, structural challenges—particularly energy shortages—are emerging as potential constraints. China, on the other hand, is steadily advancing in chip self-sufficiency and enjoys a strong foundation in power generation, giving it unique long-term advantages.

1. U.S. Advantages and Constraints The United States leads the world in foundational AI technologies, with companies such as NVIDIA, OpenAI, and Google DeepMind at the forefront of model training, algorithm development, and chip architecture. However, the rapid expansion of AI data centers has triggered significant strain on power grids. The U.S. faces increasing difficulties in meeting the electricity demands of hyperscale AI clusters, particularly in states like Texas and Virginia, where local grids are nearing capacity. Regulatory delays and environmental concerns also slow the construction of new data centers.

Moreover, while the U.S. holds a strong lead in chip design, its heavy reliance on overseas manufacturing—especially in Taiwan and South Korea—creates potential bottlenecks and geopolitical vulnerabilities. Unless domestic semiconductor production (via the CHIPS Act) accelerates substantially, this could limit the scalability of U.S. AI infrastructure.

2. China’s Growing AI Infrastructure Strength China’s AI progress has been powered by massive state-led infrastructure investments and an expanding energy base. The country’s ability to generate and distribute electricity from coal, hydro, nuclear, and renewables gives it a robust energy cushion to support energy-intensive AI development. Provinces like Inner Mongolia and Sichuan have already built dedicated data center zones designed for AI computation.

Simultaneously, China’s semiconductor ecosystem—though still behind in high-end GPUs—has achieved rapid progress in domestic alternatives. Companies like Huawei and Biren are introducing competitive AI accelerators. The Chinese government’s long-term industrial policy ensures that AI hardware, software, and application layers evolve in coordination.

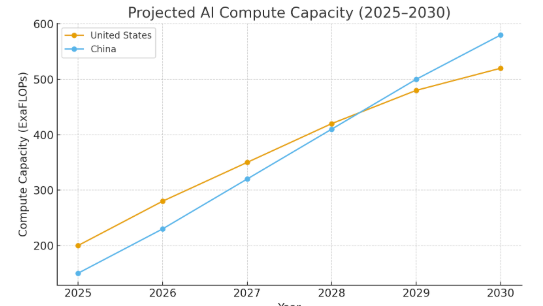

3. Five-Year Outlook (2025–2030) By 2030, the AI landscape is likely to be more balanced. The U.S. will remain the global leader in AI model innovation and ecosystem maturity, but its growth may be constrained by power limitations and supply chain dependencies. China, meanwhile, is expected to narrow the gap through a combination of energy abundance, national coordination, and local chip production.

In the next five years, the key determinant will be computational sustainability—the ability to scale AI without collapsing under energy or cost pressures. If the U.S. fails to expand its power capacity and diversify chip manufacturing, it risks losing part of its competitive edge. Conversely, if China continues to achieve progress in high-end chip design and maintains stable power support, it could become the world’s largest AI training hub.

Conclusion The AI competition between the U.S. and China will hinge not only on technological breakthroughs but also on infrastructure resilience. In an era when AI computation equals national capability, China’s abundant power and growing self-sufficiency give it structural leverage, while the U.S.’s innovative ecosystem and research leadership keep it firmly in the race. The next five years will determine whether innovation or infrastructure defines AI supremacy.